Managing money can feel overwhelming, especially when expenses seem to rise faster than income. Many people want to save more but struggle to understand how much they should spend, save, or invest each month.

That’s where the 50/30/20 budget rule comes in. Popular among personal finance experts, this simple formula provides a practical way to manage your income without tracking every rupee.

Whether you’re a salaried employee, freelancer, or someone just beginning their financial journey, the 50/30/20 rule can help bring structure to your finances.

What Is the 50/30/20 Budget Rule?

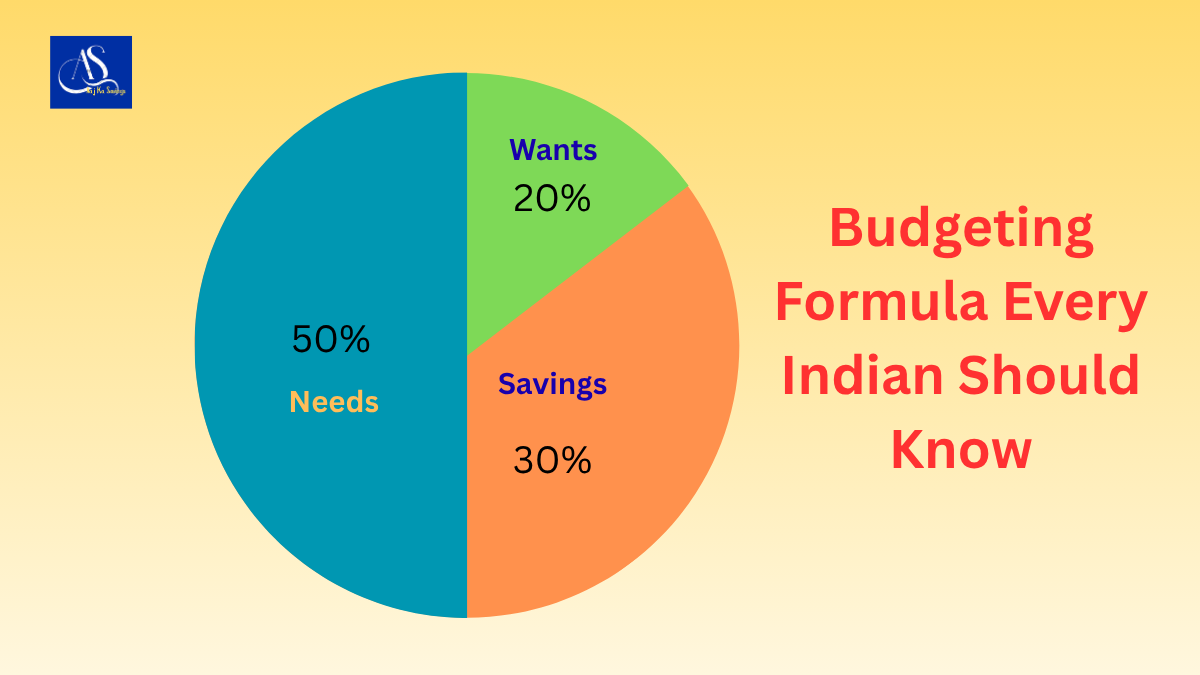

The 50/30/20 rule divides your monthly take-home income into three categories:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Investments

The goal is to ensure that essential expenses are covered, lifestyle spending remains under control, and a portion of income is consistently saved for the future.

How the 50/30/20 Rule Works

Let’s assume your monthly take-home salary is ₹50,000.

50% for Needs (₹25,000)

These are essential expenses that you cannot easily avoid.

Examples include:

- House rent

- Groceries

- Utility bills

- Transportation

- Insurance premiums

- School fees

- Mobile and internet bills

Needs are the expenses required to maintain your daily life.

30% for Wants (₹15,000)

This category includes discretionary spending.

Examples:

- Dining out

- Entertainment

- Shopping

- Streaming subscriptions

- Weekend trips

- Hobbies

The purpose of this category is to allow you to enjoy life without feeling guilty about spending.

20% for Savings and Investments (₹10,000)

This portion should go toward improving your financial future.

Examples:

- Emergency fund

- SIP investments

- PPF contributions

- Fixed deposits

- Retirement planning

- Loan prepayments

Many financial planners consider this category the most important because it helps build long-term wealth.

Why Is the 50/30/20 Rule Popular?

The rule is easy to understand and doesn’t require complicated spreadsheets.

Benefits include:

✔ Simple to follow

✔ Encourages regular saving

✔ Prevents overspending

✔ Creates financial discipline

✔ Suitable for most income levels

Unlike detailed budgeting systems, this method focuses on broad spending categories rather than tracking every transaction.

Is the 50/30/20 Rule Practical for Indians?

Yes—but with some adjustments.

In major cities like Mumbai, Bengaluru, Delhi, or Hyderabad, housing costs can consume a large portion of income.

As a result, many Indians may find a modified version more realistic:

- 60% Needs

- 20% Wants

- 20% Savings

Or even:

- 70% Needs

- 15% Wants

- 15% Savings

The principle remains the same: spend intentionally and save consistently.

Example Budget for a Salaried Employee

Monthly Income: ₹60,000

Needs (50%)

- Rent: ₹15,000

- Groceries: ₹5,000

- Utilities: ₹2,000

- Transport: ₹3,000

- Insurance: ₹5,000

Total: ₹30,000

Wants (30%)

- Eating Out: ₹4,000

- Shopping: ₹5,000

- Entertainment: ₹4,000

- Miscellaneous: ₹5,000

Total: ₹18,000

Savings & Investments (20%)

- SIP: ₹6,000

- Emergency Fund: ₹3,000

- PPF: ₹3,000

Total: ₹12,000

This structure ensures that money is allocated efficiently across all major financial priorities.

Common Mistakes to Avoid

1. Ignoring Savings

Many people save whatever remains at the end of the month.

Instead, treat savings as a fixed expense and allocate it first.

2. Misclassifying Wants as Needs

A premium smartphone upgrade may feel necessary, but it’s usually a “want.”

Being honest about spending categories improves budgeting accuracy.

3. Not Reviewing the Budget

Financial situations change over time.

Review your budget every few months to ensure it remains realistic.

Can the 50/30/20 Rule Help You Build Wealth?

Absolutely.

The real power of this rule comes from consistency.

If someone earning ₹50,000 per month saves and invests ₹10,000 monthly, they could accumulate a significant corpus over time through disciplined investing and the power of compounding.

Even small monthly contributions can grow substantially when maintained over many years.

Final Thoughts

The 50/30/20 budgeting rule isn’t about restricting your lifestyle. It’s about creating a healthy balance between spending, saving, and enjoying your income.

While the exact percentages may need adjustment based on your city, family responsibilities, and income level, the core principle remains valuable: prioritize essentials, control discretionary spending, and save consistently.

If you’re looking for a simple budgeting system that doesn’t require complex calculations, the 50/30/20 rule is an excellent place to start. It can help you take control of your finances, reduce stress, and move closer to your financial goals one month at a time.